BizAsiaLive.com is proud to introduce a brand-new column featuring Govind Shahi- ‘Media pulse by Govind Shahi’.

With over 30 years of experience in the international media industry, Govind is a highly respected expert known for his unparalleled expertise, innovative thinking, and trailblazing approach. He has been at the forefront of numerous industry firsts, consistently challenging norms and setting new benchmarks.

—

It’s surprising that channels catering to a niche audience—fewer than five million individuals—have taken this long to transition away from traditional platforms. Maintaining a presence on these platforms comes with significant costs, yet the industry has either overlooked this financial strain or given in to FOMO, doing what the others are doing and prioritising availability over profitability.

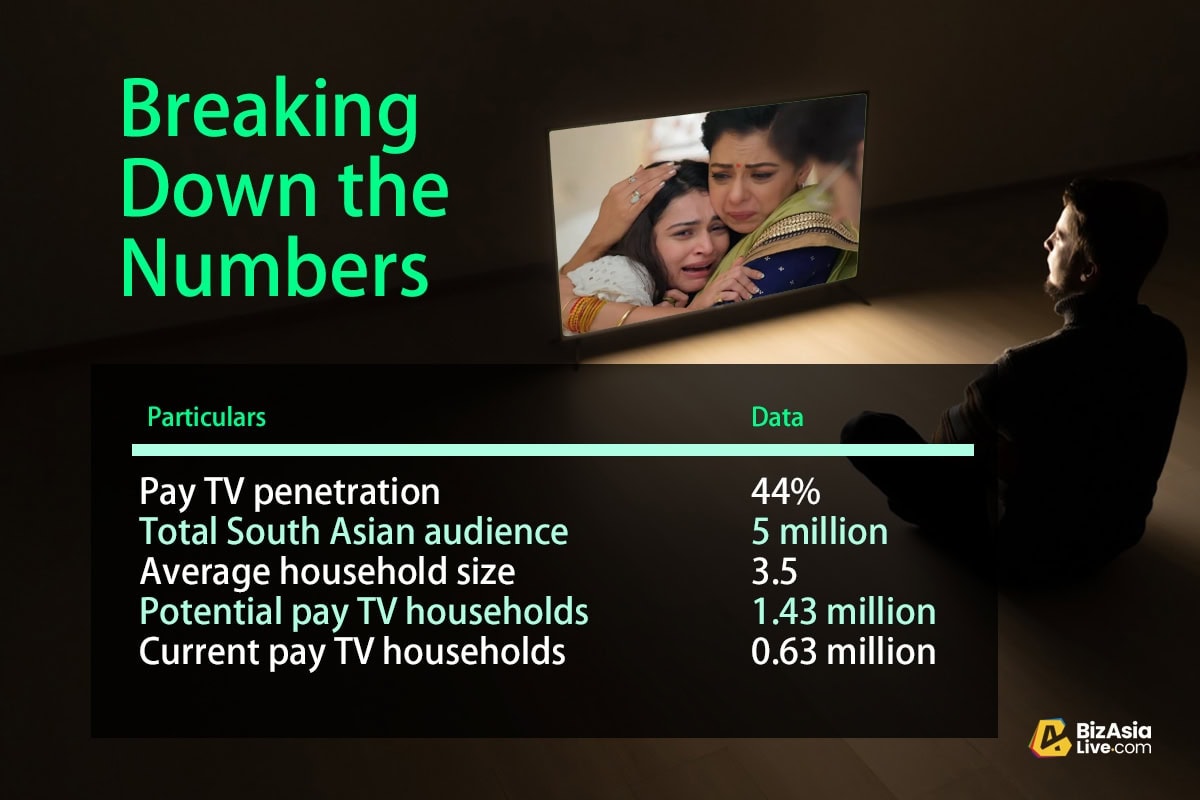

Consider this: With over 55 South Asian channels on Sky and nearly 18 channels on Virgin Media, the economics of sustaining them are questionable. If we assume a 44% pay-TV penetration rate, that translates to a total potential market of 1.43 million households. However, when we factor in real subscriptions, only 630,000 pay-TV households exist within this demographic.

Now, let’s put this into perspective: 55 channels on Sky are competing for just 630,000 households, which also have access to over 100 other mainstream and relevant channels. Meanwhile, 80% of ad revenue for larger networks relies on audience impacts, making this fragmented and shrinking market even more fragile. I’ll delve deeper into the ratings challenges in a future piece, but this alone underscores how unpredictable the advertising landscape has become. Ethnic ad revenues continue to decline, and the broader market remains volatile.

Today, it makes far more sense for channels to connect directly with their audiences—without the burden of transponder fees, EPG charges, or other legacy costs.

Historically, reaching Asian households meant securing distribution on both cable and DTH networks. But with high-speed broadband and growing acceptance of IP-based streaming, the game has changed. Today, it makes far more sense for channels to connect directly with their audiences—without the burden of transponder fees, EPG charges, or other legacy costs.

Related to this

Successful brands understand their audiences. If your viewers skew younger, they’re already embracing digital platforms. Providing seamless, on-demand access across all devices—without a subscription—can be a game-changer.

A prime example is Samar Raina’s IGL, which has successfully built viewership and generated significant subscription revenue. This proves that a direct-to-consumer (DTC) model not only boosts revenue but also dramatically cuts costs, making it a win-win strategy.

In my view, BritAsia TV is leading the charge – see this BizAsiaLive.com story, setting an example that others will inevitably follow—either by choice or by necessity. Surprisingly, the larger networks have yet to make this move, but with mergers causing channel duplication and revenue limitations making traditional distribution unsustainable, change is inevitable.

Kudos to Tony Shergill for taking the lead, moving swiftly, and setting the industry on the right path! Watch this space in the next few months.

—

Media Pulse’s goal is to spotlight the realities facing Asian media, challenges that have historically been ignored or swept under the rug. We encourage you to share your thoughts, reply, and comment. Email me govind@bizasialive.com